Saving money on car insurance with Telematics

You know you’re a good driver, so why not get all of the discounts you deserve on car insurance? By participating in your carrier’s insurance telematics program, you’ll earn 10%, 15%, even up to 30% off your car insurance premiums, automatically. Plus, you just might get some feedback that helps you maximize your discount and become an even safer driver.

What is Insurance Telematics?

Insurance is built around statistics, or the likelihood that some event may happen based on historical experience. For example, Insurance carriers know that young drivers are more likely to be involved in accidents than older, more seasoned drivers. With that knowledge in hand, they set premiums accordingly; higher for new drivers, and lower for the more experienced driver.

Age is only one determinate of driver safety though, so carriers have expanded their criteria to include other factors, such as where you live, your infractions and violations history, and even your credit score! And while they may have some statistics to support the use of these criteria, that still doesn’t tell them exactly what they need to know—are you a safe driver?

Enter Insurance Telematics; a way to verify that you really do have safe driving habits and deserve a lower rate on car insurance. With telematics, carriers no longer have to rely solely on the statistical probability that a driver will be involved in an at-fault accident, they can use predictive analytics to determine their risk. And safe drivers will be rewarded with lower premiums.

How does Insurance Telematics work?

Most of the major car insurance carriers now offer a voluntary telematics program, including Progressive with Progressive Snapshot, Safeco’s Right Track, Nationwide Smart Ride and Farmers Signal. We’ll cover some of the differences between these carriers’ offerings later, but first let’s look at how and what information they gather about your driving habits.

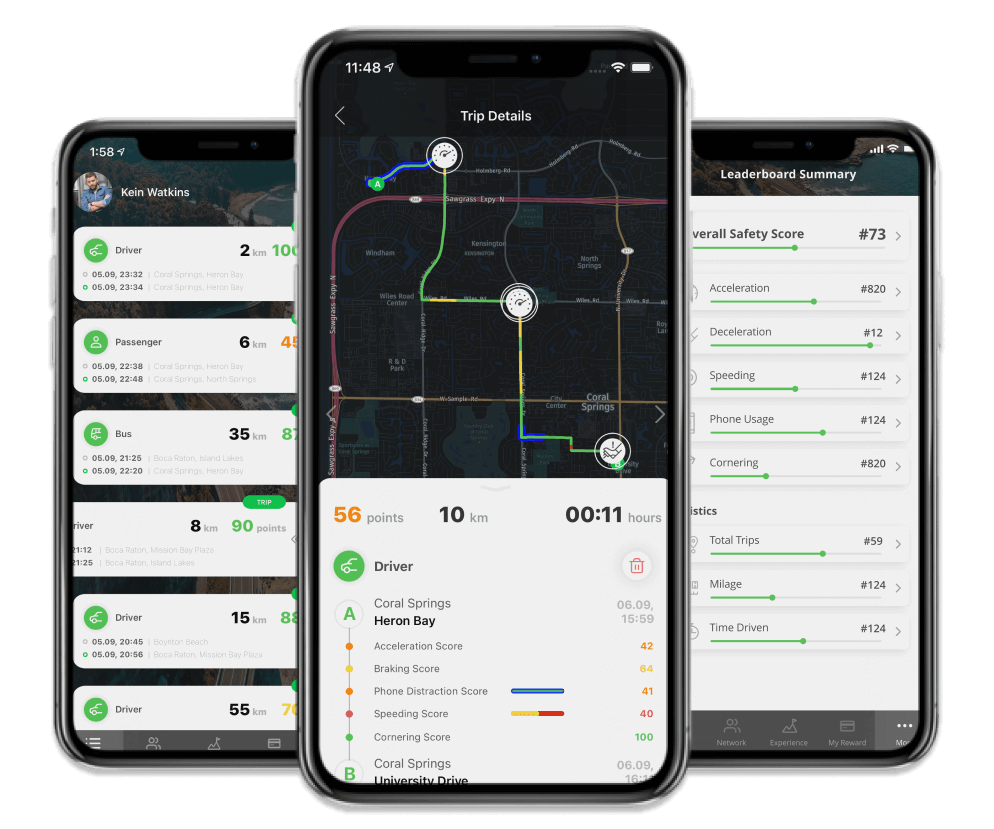

Insurance telematics rely on an electronic device in your car to measure your driving dynamics. Some carriers offer an OBD device that plugs into most cars built after the late 1990s, while others offer an app that runs on iPhones and Android phones. Both systems include sensors and GPS to track select data, then use an internet connection to send data back to the carrier for analysis.

Again, insurance telematics programs vary by carrier, and it’s important to understand exactly which factors are being tracked and weighted to calculate your telematics insurance discount. Here’s an outline of the major factors used by most companies to calculate your discounts.

Major Factors used in Telematics:

- Speed –Speeding is dangerous and sooner or later leads to a car accident. In 2019 alone, speeding was a contributing factor in 26% of traffic fatalities. https://www.nhtsa.gov/risky-driving/speeding

- Miles Driven – The less you’re on the road, the less risk you have for being in an accident. Driving even a little less can decrease your risk for an accident, lower your insurance rate, and save a little on gas money.

- Time of day driven – This factor is based on the statistic that you’re more likely to have an accident driving between the hours of 11PM and 5AM.

- Hard braking and quick acceleration – What these factors are truly looking for are avoiding following too closely and accelerating smoothly.

- Phone Usage – Distracted driving is one of the leading causes of car crashes. In 2019, 3,142 deaths were the result of distracted driving. Some carriers will include this information in the calculation of your discount. https://www.nhtsa.gov/risky-driving/distracted-driving

Your telematics program discount is personalized to your driving. And, while some programs try to auto-detect whether you are the driver or passenger on a ride, they’re not always successful. No problem, since most allow you to change your status from driver to passenger and vice versa, after the fact. That means a driving session with you as a passenger won’t count toward your telematics discount. Your discount is completely in your hands.

What else should I know about Telematics?

Telematics has benefits outside of just saving you money. You can track your own driving habits and are given tips on ways to improve your safe driving and improve your discount. What are some of the perceived disadvantages of telematics insurance? Is telematics insurance worth it?

Advantages of telematics insurance:

- Provides great discounts on car insurance premiums. – Some insurance carriers will give sign-on discounts simply for participating in the telematics program. With your safe driving habits, these discounts are increased over time. The average for these telematics discounts is around 15%-25% for consistent safe driving but select carriers give discounts up to 40%!

- Drivers determine discounts based on driving habits. – Insurance rates are based on several demographic factors that don’t really tell an insurer what type of driver you are. You may have a great driving record that gives you a reasonable rate but with telematics, insurance carriers can give you discounts based on what kind of driver you are.

- Gives insights into driving habits and ways to increase discounts. – As an already great driver, you may find you’re happy with the 15%-25% discount you receive from your insurance carriers’ telematics program. With the telematics program, insurance carriers will provide insights for improvements to your discount based on your ride history.

Perceived disadvantages of telematics insurance:

- Track your location and driving habits – One of the perceived disadvantages of your insurance carrier’s telematics program is that they track your location and driving habits. The information collected from these programs is sent through a private secure network. This is then anonymized and used for the statistical risk assessment that calculates the discount you receive.

- Vague Criteria/Lack of Transparency – Some of the factors that contribute to your insurance discount are not clearly defined. Factors like “hard-braking”, or “quick acceleration” are based on your insurance carrier’s definition. To understand the specifics of this, you want to speak with your insurance carrier to understand how they define these factors.

- Some telematics insurance carriers track factors outside of the driver’s control – One of the factors like driving at night are outside of what you control behind the wheel. If you work a swing shift and would like to participate in a telematics program, make sure to discuss with your agent if this will be used in your discount calculation.

Taking Action on Insurance Telematics

If you are an already safe driver, a driver looking to improve, or you just want to earn discounts based on your driving, telematics could be a great option for you. If you would like more information about your carrier’s telematics program, our FAQ section and links below give more specified information on Telematics. You can also contact Phoenix Insurance Inc. for recommendations based on your specific needs.

Frequently asked about Telematics

Should I join a telematics program?

Well, it depends; if you’re a good driver looking for savings on car insurance, then absolutely. We’ll help you choose a carrier that offers a program that’s right for you.

What does the Smart Ride Nationwide App define as braking too hard?

While most carriers don’t publish the exact criteria for what they consider “hard braking”, many safety experts use 15 ft/sec2 (0.47 G’s) as the maximum deceleration that is safe for the average driver to maintain control, with good to excellent tires on a dry surface.

What does Progressive Snapshot define as accelerating too fast?

Safety experts generally view harsh acceleration as anything generating over 0.43 G’s, or the equivalent of accelerating from a standstill to 37 mph in 3.95 seconds. Progressive Snapshot and other telematics programs generally use this type of data to benchmark drivers’ performance.

Why does Progressive Snapshot track speed?

As with all insurance telematics programs, Progressive’s Snapshot tracks speed as a key indicator of driver safety. Higher speeds offer the driver less reaction time, and exponentially increases the damage, both vehicular and human, of any resulting collision.

What does Nationwide Smart Ride track?

All carriers are constantly refining their telematics programs, so this information can change, but a recent Consumer Reports review includes Braking, Time of Day, Distance, Acceleration and Other factors of data tracked by Nationwide Smart Ride.

What are the differences in telematics programs; How should I compare telematics insurance programs?

With dozens of options out there and little in the way of details, comparisons can be difficult. Use your existing carrier’s web pages as a starting point, then benchmark your findings against other carriers that offer similar products that fit your needs.

Can Progressive Snapshot track your location?

Some insurance telematics programs employ geofencing or other GPS techniques to track your location, but Progressive Snapshot is not one of them.

Can I use a telematics device for car insurance instead of my phone?

Check with your carrier (or independent agent) to see if they support the use of OBD devices for their telematics program. An OBD device plugs into most cars built after the late 1990s and does not require you to install an app on your phone.

Where does this information go?

Each carrier maintains their own cloud-based secure server which collects the data sent by drivers’ devices. See an individual carrier’s privacy policy for their detailed use or ask your agent.

How does Progressive Snapshot know I’m a passenger?

Regardless of claims to the contrary, insurance telematics apps aren’t that great at distinguishing whether you’re the driver or a passenger in the vehicle. Progressive Snapshot and others employ a variety of sensors in your phone to try to establish if you’re the driver, but users report mixed results. Fortunately, most apps allow you to correct any rides where they misclassified your trip.

E&OE. All trademarks are trademarks or registered trademarks of their respective owners and are used here in accordance with the fair use doctrine of the US Copyright Act. This is work is Copyright © 2022 Phoenix Insurance Inc. – All rights reserved.